An injury insurance claim can be the difference between financial stability and crisis when a professional athlete's career is interrupted. Yet the process is poorly understood by most players — even those earning millions. Knowing exactly what to do, when to do it, and how to document everything correctly can mean the difference between a successful payout and a denied claim. This guide walks you through the entire process.

Step 1: Understand What Your Policy Actually Covers

Before you are ever injured, you need to know your policy inside out. This sounds obvious — but the majority of professional athletes, including many in the Premier League, La Liga, and the NBA, have limited understanding of the specific terms of their insurance coverage. The most important things to know:

- Definition of disability: Does "total disability" mean unable to play any sport, or unable to play your specific sport at professional level? The difference is enormous.

- Covered activities: Are training sessions covered? What about national team duty? Pre-season tours abroad? Each policy is different.

- Exclusions: Pre-existing conditions, recreational activities, and injuries sustained outside of sanctioned sport are common exclusions.

- Notification period: How long do you have to notify the insurer after an injury? Typically 30 to 90 days. Breach this and your claim may be void.

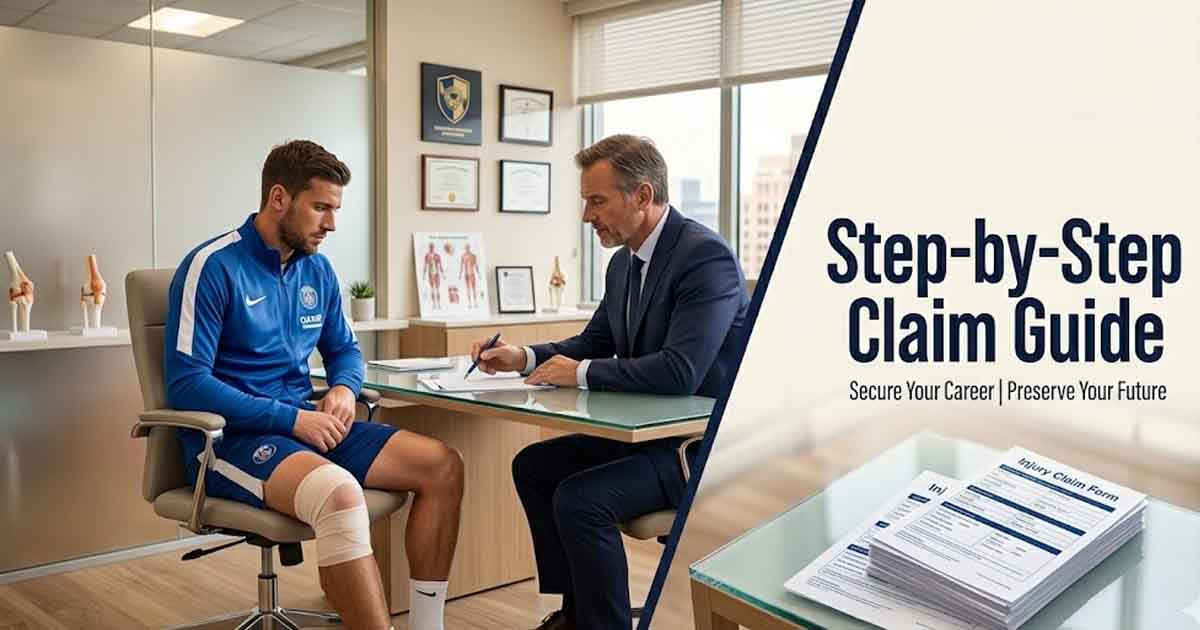

Step 2: Notify Your Insurer Immediately

The moment you sustain a significant injury, contact your insurance broker or insurer — before you even have a confirmed diagnosis. Early notification protects your claim. Most policies require notification within a specific window, and waiting for scan results or a surgeon's opinion before making contact is one of the most common and costly mistakes athletes make. A simple notification call costs nothing and preserves your right to claim.

How Injured Athletes Like Ibrahimovic Managed the Process

Zlatan Ibrahimovic, who suffered a serious ACL injury at Manchester United at the age of 35, demonstrated how experienced athletes handle injury — both physically and financially. Ibrahimovic's team initiated insurance proceedings immediately, secured independent medical assessment, and maintained detailed documentation throughout his recovery. He returned to professional football less than a year later and continued playing until his mid-40s — but his financial protection during that period was handled with the same professionalism as his rehabilitation.

Compare that to players who delay, assume the club is handling everything, or fail to engage a personal adviser. The difference in financial outcomes is significant.

Step 3: Build Your Medical Documentation File

Your insurance claim is only as strong as your medical documentation. Insurers will scrutinise every piece of evidence before approving a significant payout. Your file should include:

- Initial injury report from the attending medical professional

- All imaging results (MRI, CT scan, X-ray) with radiologist reports

- Surgeon's assessment and recommended treatment plan

- Independent medical opinion (not just from the club doctor)

- Detailed rehabilitation timeline and progress reports

- A clear prognosis: expected return date or declaration of permanent inability

Getting an independent medical opinion — separate from the club's medical team — is especially important. Club doctors serve the club's interests. For personal insurance claims, your documentation needs to serve your interests.

Step 4: Calculate All Income Lost

A common error is calculating the claim solely around base salary. For professional athletes, income is multi-layered. Your claim should account for:

- Base salary lost during the injury period

- Match appearance fees and performance bonuses

- Prize money or competition bonuses missed

- Endorsement income affected by availability or performance clauses

- Image rights payments suspended due to injury

- Rehabilitation and medical treatment costs

For players like Marcus Rashford or Raheem Sterling, endorsement income can represent a substantial portion of total annual earnings. Failing to include this in the claim calculation means leaving significant money unclaimed.

Step 5: Engage a Sports Insurance Specialist

For any claim above £100,000 — which for most professional athletes means virtually any significant injury — engaging a specialist sports insurance lawyer or claims consultant is essential. These professionals understand policy language, know what insurers look for, and can negotiate on your behalf. The cost of their service is almost always recovered in the improved settlement they achieve.

What Happens if Your Claim Is Disputed?

Insurers dispute claims. It happens. If your claim is rejected or disputed, you have several options:

- Internal appeal: Request a formal review through the insurer's appeal process.

- Independent medical arbitration: Many policies include provision for independent medical review of disputed disability definitions.

- Financial Ombudsman: In the UK, the Financial Ombudsman Service provides a free dispute resolution service for personal insurance disputes.

- Legal action: For large claims, litigation against an insurer — while expensive — is sometimes the only route to a fair settlement.

Final Checklist for Athletes

Before you ever need to make a claim, make sure you have:

- Read and understood your current policy in full

- Confirmed your coverage includes training, national duty, and all relevant activities

- Stored your policy documents and broker contact details where you can access them immediately

- Briefed your agent or manager so they can act quickly on your behalf if you are incapacitated

- Reviewed your policy annually as your income grows

An injury is a crisis. The claims process does not have to be. Preparation is everything — and the athletes who come out of injury financially intact are the ones who treated their insurance with the same professionalism they brought to their sport.

Add a Comment